Choosing between owning a mobile home and renting an apartment is a major housing decision. To help people make an informed choice, we conducted a detailed analysis comparing the financial aspects of renting an apartment and owning a mobile home in two mobile home communities: Villa Diann Eau Claire and Hillcrest Estates in Altoona, Wisconsin For the detailed analysis, click here: Buying a MH vs Renting Numbers

For our analysis, we are assuming the following. A 3-bedroom mobile home price is 100k with tax. Down payment is 10k. Interest rate is 9% for 25 years. Lot rent is $400 a month and increases 4% per year. Home appreciates 2% per year. 3-bedroom apartment rent is 1,500 a month and increases 4% per year. We believe these assumptions are conservative. We are not comparing utility costs, though many mobile home home buyers report savings due to better insulation.

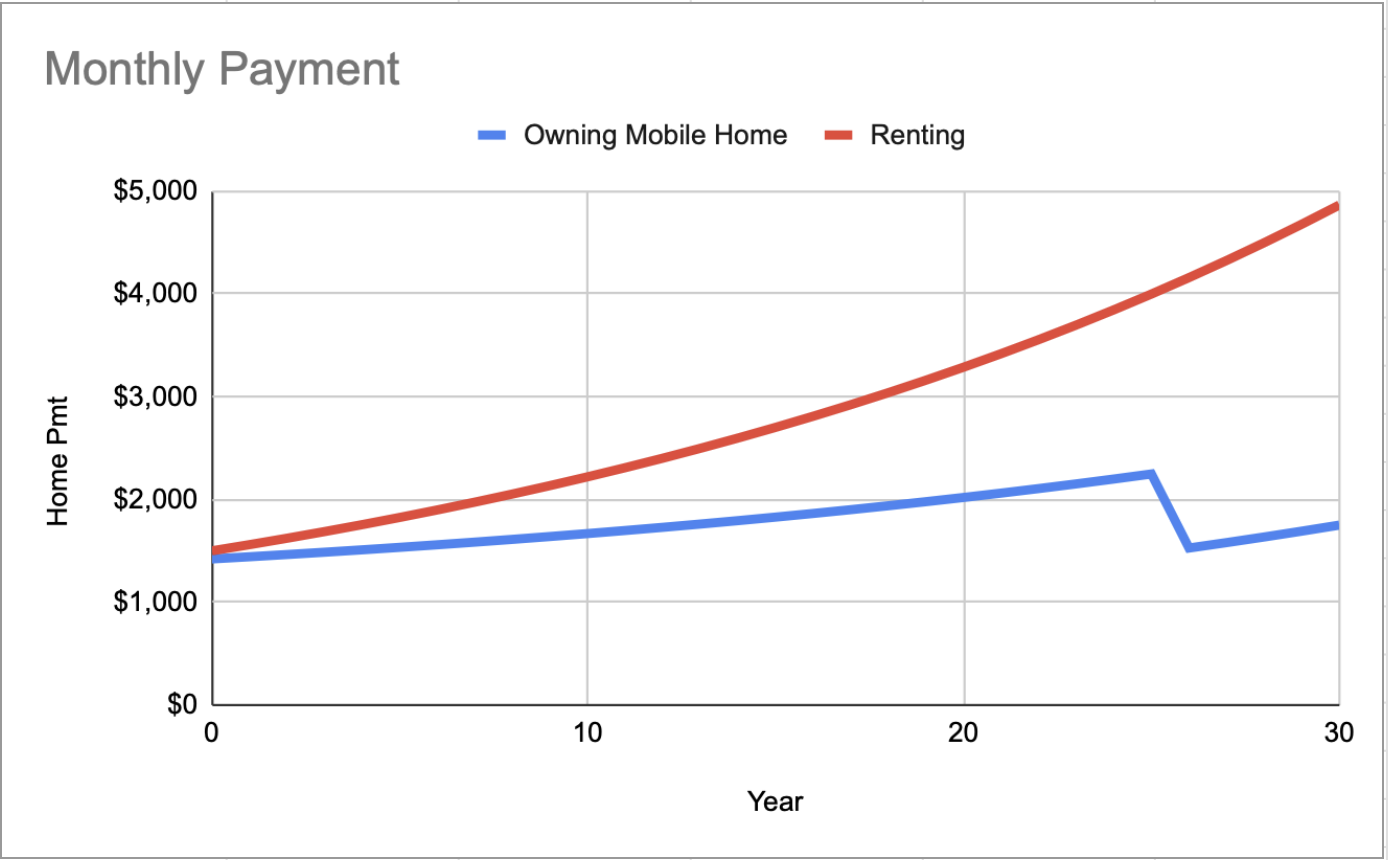

Apartment Rent Can Increase Faster than Mobile Home Payments

Owning a mobile home involves an initial down payment, monthly home loan payments, lot rent, tax, and insurance. Remarkably, these monthly payments can be comparable to renting an apartment. However, the key difference lies in these costs over time.

For mobile home owners, the loan payment usually remains constant for the duration of the loan. This is because most loans have fixed interest rate for a fixed amount.ax and insurance increases are gradual. However, when it comes to apartment rent it often sees an annual increase, making the overall cost of renting significantly higher as the years and sometimes months go by!

Buying a mobile home ($1,421) and renting ($1,500) start off at similar monthly payments. Over time, however, the difference becomes significant. By year 5, renting cost about $300 more per month. In 10 years, renting costs $550 more per month. If you continue renting, you can pay over $1200 more in year 20.

Monthly Payment:

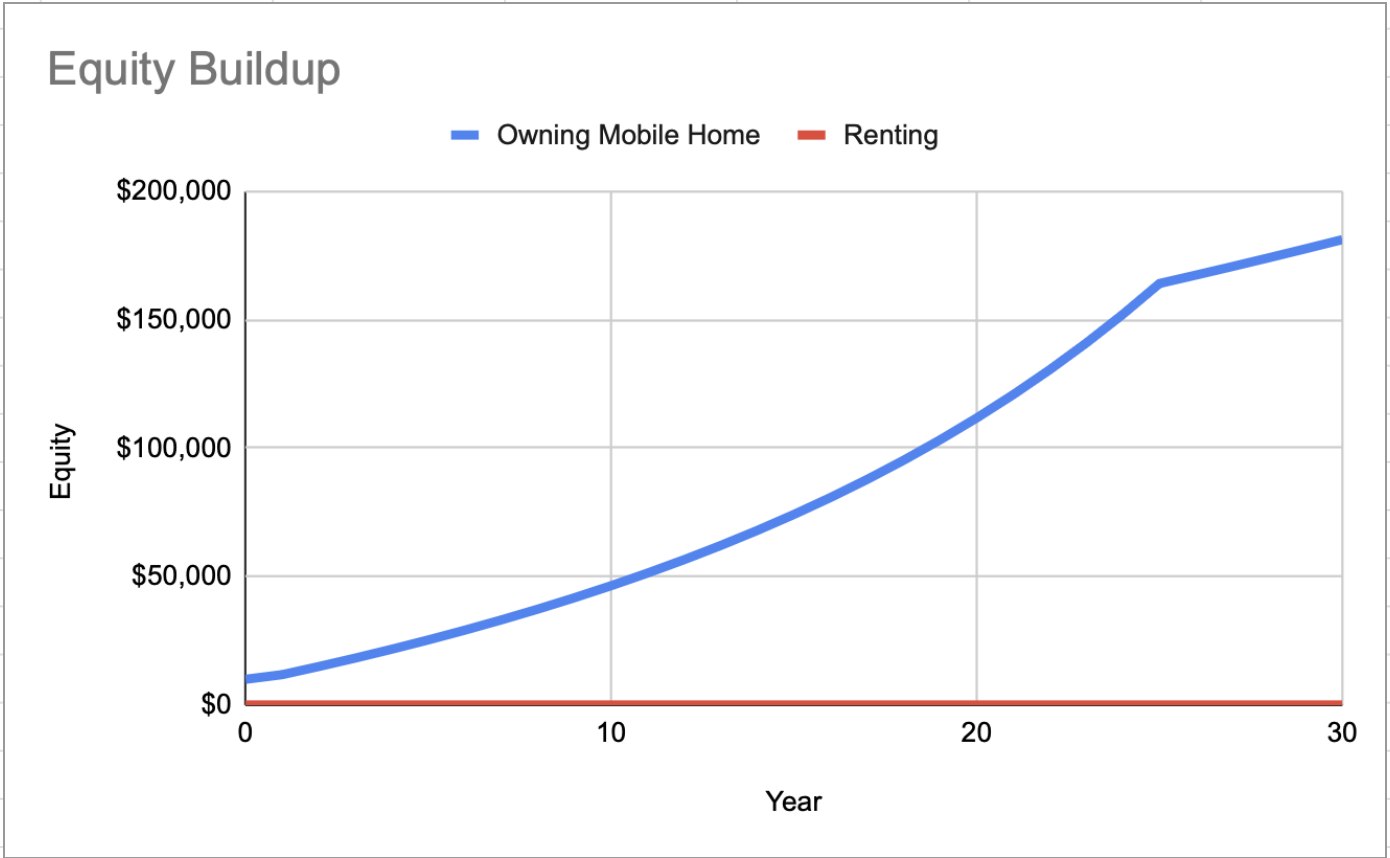

You Can Build Equity with Mobile Homes.

One of the greatest advantages of owning a mobile home is the equity it builds over time.

When you purchase a mobile home with financing, you are paying down the loan while the home value appreciates. In contrast, when you rent, you do not get any equity. You are helping your landlord build their equity.

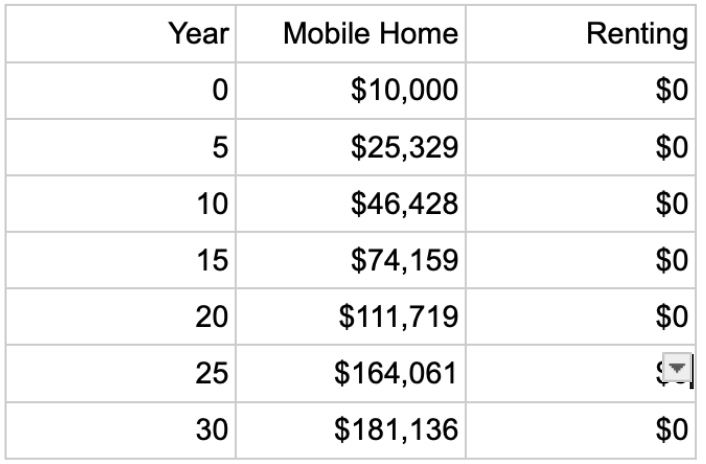

In our analysis, by the fifth year, homeowners have accrued $25k in equity. This includes the initial $10k down payment and $15k in equity buildup. Looking further ahead, the equity skyrockets to $46k by year 10 and an impressive $181k by year 30. Renting an apartment leaves residents with zero equity. There is a chart that shows a visual representation of the data we found below.

Equity:

Other Advantages of Mobile Home Ownership

Beyond the financial considerations, mobile home ownership offers a range of lifestyle advantages. These include:

1. Homeownership Benefits: Enjoy the pride and stability that comes with owning your own home.

2. Increased Privacy: Mobile homes typically provide more privacy than apartment living.

3. Stability: Avoid the hassle of frequent moves and the uncertainty of changing rental markets.

4. No Shared Walls: Experience the freedom of living without shared walls with neighbors.

5. Freedom to Customize: Unlike rental apartments, mobile homeowners have the freedom to personalize their living space.

6. Quality Living: Many mobile homes are well-insulated, resulting in potential savings on heating and cooling costs.

7. Cost Effective, you aren’t having to move apartments to find a better rate so you end up saving the moving cost you would have spent without owning a home.

While the choice between renting a mobile home and an apartment is a difficult one, our analysis sheds light on the financial advantages of mobile home ownership, especially in the long term. Beyond the financial aspects, the additional benefits make mobile home living an attractive option for those seeking stability, privacy, and the pride of homeownership. Hillcrest Estates and Villa Diann take pride in our residents and would love to help you find your next home!